Does your business provide meals and entertainment for employees, clients/customers, or partnership representatives? How the IRS allows businesses to handle meal and entertainment costs in relation to their taxes has had quite a few changes over the last few years. The 2018 Tax Cuts and Jobs Act (TCJA) eliminated deductions for most business-related entertainment expenses. And now since the pandemic, the IRS temporarily changed the tax-deductible amount allowed for some business meals to encourage increased sales at restaurants. With the easing of restrictions, your leadership may be considering company picnics for employee appreciation or starting up business lunches with clients again.

Given all of these changes, putting a system in place to accurately track business food and entertainment expenses becomes essential. Best practices should include requesting detailed receipts and separately tracking which costs fall under the 50 percent deduction, 100 percent deduction, or not deductible categories. Training team members who handle the food and entertainment charges will help your bookkeeping team, as well.

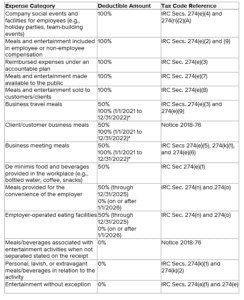

In addition to keeping excellent records, below are some additional things to keep in mind about the business meal and entertainment deduction rules, including a helpful chart highlighting the deduction category particular meal and entertainment expenses fall under.

Meal and entertainment expense changes

Under the TCJA, the IRS no longer allows businesses to deduct most entertainment expenses even if they were a cost of doing business. Food and beverage related to entertainment venues are only covered with detailed receipts separately stating the price of the meal.

Another change from the TCJA is that spouse or guest meals are not covered from travel unless the business employs the person. So, if your spouse accompanies you on a work trip, their meals are not deductible for the business.

The Consolidated Appropriations Act of 2021 (CAA) temporarily increased the deduction for business meals provided by restaurants to 100 percent for tax years 2021 and 2022. Not all meals are created equal, however. The 100 percent deduction is only available for meals provided by restaurants, which the IRS defines as: “A business that prepares and sells food or beverages to retail customers for immediate consumption, regardless of whether the food or beverages are consumed on the business’s premises.” Prepackaged food from a grocery, specialty, or convenience store is not eligible for the 100% deduction and would be limited to a 50% deduction.

Also, as has always been the case, expenses must be considered ordinary (common and accepted for your business) or necessary (helpful and appropriate) and cannot be considered lavish or extravagant. An employee of the business or the taxpayer must be present during the meal, as well.

A quick guide to business meal deductions

*Meals are only deductible in the 2021 and 2022 tax years if provided by a restaurant, as defined by the IRS in the above article.

Entertainment expenses are notoriously targeted by auditors. Considering the law change, we anticipate these expenses to be a heightened area of concern during an audit. The professionals in our office can help ensure you are in compliance, call us today.

If you have additional questions as it relates to meal and entertainment deductions or need help creating a system to track expenses or seek clarification on whether certain expenses are tax-deductible, Selden Fox can help. For additional information please call us at 630.954.1400 or click here to contact us.